Following my last column Predictions 2026: The Revenge of Common Sense in the West, a questionable assertion emerged: that the United States grew because public spending increased. This claim requires a more careful evaluation: analyzing what type of spending grew, why, and what truly drove U.S. economic growth in 2025.

It is true that federal public spending increased in nominal terms. The mistake lies in accepting the figure without breaking it down. The thesis of this article is that U.S. growth occurred despite the drag of inherited expenditures and thanks to a more disciplined orientation in fiscal management, employment, and economic incentives.

A first argument consists of equating an increase in public spending with deliberate State expansion. If we observe the real composition of federal outlays, we can distinguish between discretionary spending and inertial spending. In the language of U.S. public finances, outlays represent the spending effectively executed by the federal government during a fiscal year. They include both mandatory payments—pensions, healthcare, and debt service—established by law, as well as discretionary spending—defense, civilian agencies, and operational programs—that depend on political decisions. This distinction is key, since a significant portion of spending responds to inherited commitments that the government is obligated to honor, regardless of its economic orientation.

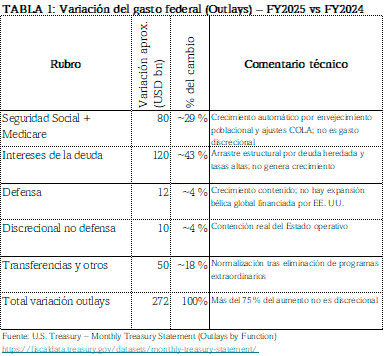

According to data from the Monthly Treasury Statement, broken down in Table 1, the increase in federal spending between fiscal years 2024 and 2025 was 272 billion dollars. However, more than 70% of that increase was concentrated in mandatory compliance items. Debt interest accounted for approximately 43% of the total increase, reflecting the drag of accumulated deficits and still-elevated interest rates. Added to this was the automatic growth of Social Security and Medicare, contributors of 29%, driven by population aging and mandatory inflation adjustments. By contrast, discretionary spending—both in defense and civilian programs—showed a variation of less than 10% of the total increase, reflecting real spending restraint that did respond to executive control.

Table 1:

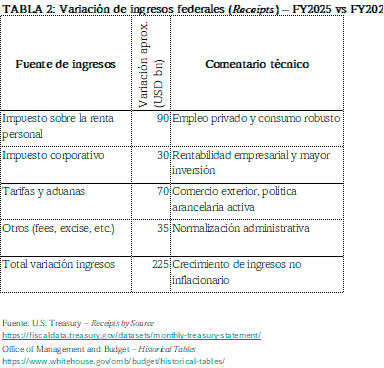

The next point in the fiscal debate is usually revenues. Data from the Monthly Treasury Statement, summarized in Table 2, show that between fiscal years 2024 and 2025 federal revenues increased by approximately 225 billion dollars. This growth was the result of an expansion of the real economic base. Personal income tax explained approximately 90 billion dollars of that increase, a direct reflection of greater private employment and sustained consumption. Corporate tax contributed another 30 billion dollars, signaling business profitability and greater productive activity.

Particularly relevant was the growth in tariff and customs revenues, which added approximately 70 billion additional dollars. This category, linked to effective foreign trade and an active tariff policy, represented nearly one-third of the total increase in revenues. Added to this were other administrative and special revenues, resulting from normalization in tax collection. In conclusion, the strengthening of revenues in 2025 responded mainly to greater private activity and real trade.

Table 2:

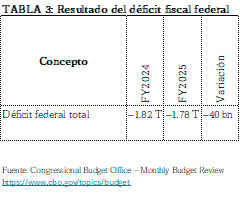

Now then, if federal spending increased and revenues grew less than outlays, how is it explained that the fiscal deficit was reduced? The answer lies in budgetary arithmetic. Data from the Congressional Budget Office, synthesized in Table 3, show that the federal deficit went from approximately 1.82 trillion dollars in fiscal year 2024 to around 1.78 trillion in 2025, a reduction close to 40 billion.

Table 3:

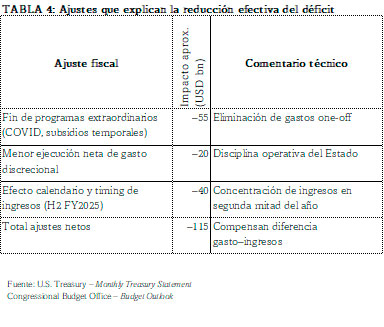

This result is explained through concrete adjustments, detailed in Table 4. First, the end of extraordinary programs inherited from the pandemic and temporary subsidies eliminated around 55 billion dollars. Second, the lower net execution of discretionary spending—both civilian and operational—contributed an additional adjustment close to 20 billion. Finally, calendar effects and the timing of revenues concentrated in the second half of the fiscal year explained another 40 billion. Without these three factors, all dependent on a different fiscal orientation, the deficit would have increased.

Table 4:

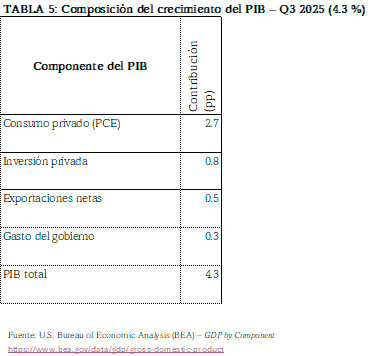

Then arises the central question: if it was not public spending, what truly drove U.S. economic growth in 2025? According to data from the Bureau of Economic Analysis, broken down in Table 5, GDP growth in the third quarter of 2025—4.3% annualized, and one of the highest in the world—was clearly dominated by the private sector. Personal consumption explained approximately 2.7 percentage points of total growth, sustained by private employment and consumer confidence. Added to this was private investment, which contributed around 0.8 percentage points, signaling favorable expectations and greater business willingness to commit capital. Net exports contributed around 0.5 points, while spending by the federal, state, and local governments contributed barely 0.3 percentage points.

Tabla 5:

This composition is decisive for understanding the nature of the observed growth. It was not an expansion driven by fiscal stimulus or massive public spending, but rather a dynamic led by private consumption and investment, with the State accompanying only marginally.

To this retrospective reading is added a relevant prospective signal. Real-time projection models such as the Federal Reserve Bank of Atlanta’s GDPNow estimated at the end of December 2025 that real GDP growth in the fourth quarter could reach an annualized rate close to 5.4%, far above initial forecasts. It is not a definitive official figure, but its importance lies in the direction indicated: an additional acceleration of growth driven once again by private components, not by public spending. If confirmed, this result would reinforce the interpretation that the 2025 expansion was neither an isolated rebound nor a fiscal artificiality, but rather a dynamic consolidated throughout the year. Imagine what could happen if this trend were maintained over the next three years.

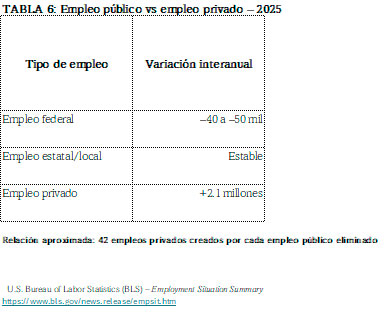

The labor market provides additional confirmation. Data from the Bureau of Labor Statistics, summarized in Table 6, show that throughout 2025 federal employment decreased by an estimated range of 40 to 50 thousand positions, while the private sector created approximately 2.1 million new jobs during the same period. The resulting ratio—around 42 private jobs created for every public job eliminated—does not describe a contraction of the labor market, but rather a reallocation. State adjustment did not push workers into unemployment; the market absorbed them quickly, signaling an economy capable of generating opportunities without depending on the public budget as the principal employer.

Table 6:

The evidence from 2025 shows that growth did not come from an expansive State, but from a restraint on spending, allowing the private sector to do its work. Public spending was contained, revenues increased, and the deficit began to correct itself due to its fiscal orientation. The result was a growing economy, creating private employment and capable of recovering dynamism in an adverse international context.

This evidence confirms that the republic functions when the State is strong in what is essential and prudent in everything else; when it does not replace the citizen or the enterprise, but instead guarantees rules, stability, and responsibility. For countries such as Guatemala, trapped between the temptation of populism and the inertia of inefficient statism, the lesson is clear: sustainable growth is not born from the budget, but from economic freedom, productive work, and fiscal discipline. That is, ultimately, the true common sense that the West is beginning to recover today.

Ramiro Bolaños, PhD. / President of the Center for Thought and Action: Factoría Libertatis